Exports of waste from the UK to continental Europe in recent years have soared. The additional volumes have been a major factor in stabilising market conditions in countries such as the Netherlands and Germany. With energy-from-waste (EfW) becoming an appealing stable asset class, merger and acquisition (M&A) activity has picked up.

Throughout this century, the UK government has advocated landfill diversion policies: in 2010, 85% of residual waste was landfilled versus 50% in 2016. The UK government introduced an increasing levy on landfilling residual waste and financial support for the Waste Private Finance Initiative resulted in the development of more EfW plants.

Consequently, the UK experienced a considerable growth in incineration capacity with an installed and operational base of around 10 million tonnes by the end of 2016 which is projected to increase to around 15 million tonnes by 2026. Furthermore, the Environmental Services Association (ESA), representing waste management companies, has concluded that the UK is heading for serious under-capacity for residual waste treatment.

At the industry consensus of a 50%-55% municipal recycling rate, the forecast treatment capacity gap is expected to be almost six million tonnes in 2030 with regional differences predicted to further aggravate this capacity shortfall.

Stabilising impact on continental European markets

During the last economic crisis, major continental European waste markets, such as the Netherlands, faced substantial pressure on gate fees as residual waste volumes dropped and competition became fierce for local waste volumes; in the Netherlands the local overcapacity drove municipal gate fees to levels as low as EUR 35- EUR 45 per tonne.

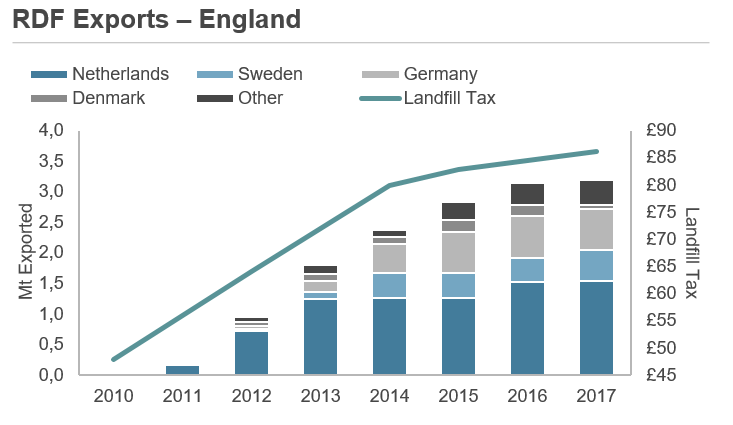

UK exports of refuse-derived fuel (RDF) developed substantially while capacity in northwest Europe became scarce and incineration fees continued to rise.

There is uncertainty about future incineration capacity. As a result, waste suppliers are attempting to renew waste intake contracts over longer periods with higher gate fees, often years before the existing contracts expire, to secure future off-take. A recent example was between Renewi and AEB: a 10-year off-take contract to supply RDF to AEB’s facility in Amsterdam. Renewi will send up to one million tonnes of RDF from east London.

Waste-to-energy capacity

The key factor is the market’s expectation of the future EfW capacity in the UK. The development of additional incineration capacity in the UK has proved to be coming progressively more difficult, demonstrated by the fact that since December 2016 only one new facility has been announced.

Underpinning this development is the project finance requirement for a significant proportion of capacity to be contracted on a long term. This has become a challenge because most of the UK’s municipal residual waste is already covered by existing capacity. The remaining commercial and industrial waste can only be secured with contracts maturing between three and five years, requiring project sponsors to finance such new builds “on balance sheet”. Other factors include the EUR/£ exchange rate, Brexit uncertainty, future volumes and the capital cost of new energy. These concerns seem to have calmed partly because the UK government is developing a resource and waste strategy and remains committed to landfill diversion.

Role of infrastructure funds

With the strong market conditions, robust outlook, and long-term feedstock contracts, infrastructure funds have become increasingly attracted to EfW in their quest for stable yields. Combined with considerable appetite from lending banks and a competitive cost of equity, this has led to several M&A transactions. With a strong outlook expected for the short-medium term, further similar M&A activity can be anticipated in the coming years.

This article was written by Laurens van Asselt, a managing director in Houlihan Lokey’s Corporate Finance business.

Don't hesitate to contact us to share your input and ideas. Subscribe to the magazine or (free) newsletter.