‘Prices for lithium, cobalt and nickel underscore the likely skepticism about the timing and magnitude of the new energy revolution,’ report analysts at FastMarkets.

The trailing 24 months show a steady decline in prices. ‘Lithium surpluses over the past 12 months months alone have caused prices to drop by 41% for lithium carbonate and by 32% for lithium hydroxide monohydrate,’ analysts note.

The low prices and weakened demand have put the brakes on new supply, alongside cutbacks of existing supply – meaning the market is beginning to rebalance while excess inventory gets used up. Looking ahead; lithium demand is expected to more than triple, to 940 000 tonnes from 300 000 tonnes in the next five years.

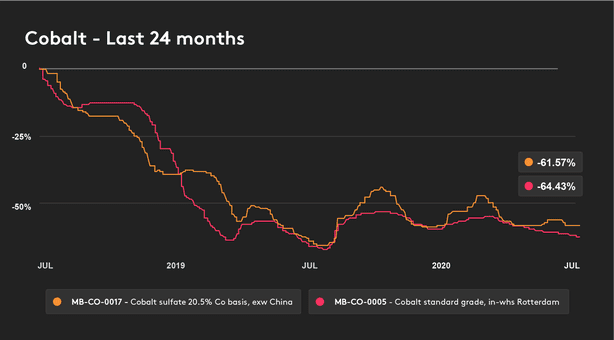

Meanwhile, cobalt fell from near 10-year highs in April 2018 to pre-Covid lows in July 2019. Recent prices are slightly above those lows, at US$ 14 per lb. ‘It has been a rocky road: cobalt hydroxide prices rose in May due to supply disruptions caused by a lockdown in South Africa aimed at containing the spread of the Covid-19 virus, but prices took a hit in early June when interest in spot buying thinned,’ analysts write.

Prices have remained under pressure during the third quarter of 2020 due to weak downstream demand. However, it is anticipated that cobalt demand will increase by 55% in the next five years.

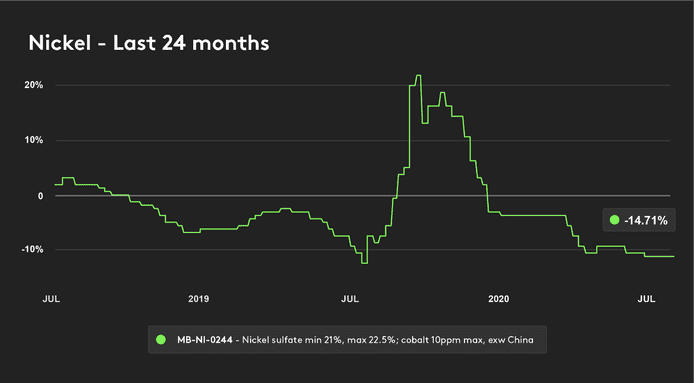

As for nickel, demand from batteries is expected to grow by over 150% in the next five years, to 400 000 tonnes from 150 000 tonnes. While most nickel is used for stainless steel (only 5% of nickel goes into electric vehicles) and lithium iron phosphate batteries are gaining share, nickel remains a priority material for batteries while companies explore new chemistries.

Even though stainless steel demand has been steady, there has been some volatility over the past couple of years. ‘Nickel prices rose in October 2019 amid concerns about supply stemming from an Indonesian ore ban, but took a hit as Tesla decided to use lithium iron phosphate batteries in its Model 3 in China,’ it is observed.

How to prepare for resource competition?

- Expand recycling to grow supply;

As more batteries come to the end of their useful life, companies like Umicore and Neometals are building recycling capabilities to prepare for high-growth demand and the need for recycled materials.

- New lithium mining and extraction methods;

Even against the backdrop of falling prices, companies are exploring new extraction techniques to improve yield from 30% to 70% and some governments are considering urban mining to grow demand and enable localized supply chains.

- Extend upstream into the supply chain;

Automotive brands are getting directly involved in lithium and cobalt procurement rather than letting the battery companies do it for them.

- Put in place off-take contracts;

Cobalt buyers are locking in four to five-year contracts to ensure their allocation from miners. Alternatively, buyers benefit from assured supply while producers ensure liquidity while demand finds it footing.

Read the complete report here.

Don't hesitate to contact us to share your input and ideas. Subscribe to the magazine or (free) newsletter.