Page 61 from: Recycling International May/June issue

61recyclinginternational.com | May/June | 2025

the EU: With net exports of 7.6 mil-

lion tonnes, Europe remains a signifi-

cant supplier. ‘Paper mills rely on

imports because the internal market

collection system cannot meet

demand,’ Hayes observes.

European legislation is increasingly

complicating international trade in

recovered paper, he told delegates.

For example, the new EU Waste

Shipment Regulation, which will apply

from May 2027, will significantly

impede the export of non-hazardous

waste to third countries. The industry

says the law remains unclear, so it has

had to do its own research.

Hayes points out that, thanks to the

European umbrella recycling associa-

tion EuRIC, key importing countries

had completed the necessary regis-

trations with the European

Commission in time. ‘I’m very thankful

to EuRIC that it was able to talk some

sense into EU legislators at the 11th

hour regarding volume quota.’

QUALITY IS KEY

Though the quality of recovered

paper in Germany and other leading

European countries is high, Hayes

says the legal classification of when

paper is waste is an unresolved prob-

lem. ‘Despite years of efforts, there is

no uniform recognition as a product.

Inconsistent regulations across

Europe complicate trade and spark

uncertainty.’

Negotiations on an EU-wide end-of-

waste proposal for paper failed in

March 2025 but the industry is hoping

for progress at national level. ‘As it

stands, recyclers are hitting a lot of

bureaucratic walls.’

At the same time, the quality of

recovered paper is declining due to

economic developments and new

forms of packaging. Fibre-based com-

posite packaging, in particular, com-

plicates recycling and hampers recy-

cling from blue bins.

Hayes concludes that the key to suc-

cess is transparency, shared ambition

and keeping an open dialogue. ‘Every

day we are bombarded with worrisome

headlines about politics. We need to

respect each other, even if we disagree.

The world is getting out of hand and

RECOVERED PAPER

it’s easy to get caught up in that nega-

tive energy. It’s a shame and it distracts

us from what really matters.’

NORTH AMERICAN MARKET

During her presentation, McNamara

also reviewed the North American

recovered paper market over the last

15 years, pointing out that demand

for containerboard has been consis-

tent (up 1.2% since 2009) while

graphic paper demand has been in

decline (down 7%).

Of the main grades globally, demand

for high grades has been decreasing

more slowly in North America over

the last decade. In 2014, demand was

12.4 million tonnes, while it was just

7.0 million tonnes last year, an annual

dip in supply of 5.3%. But both in

North America and the export mar-

ket, high grade demand from mills

has dropped only 1.3% over the

same period. ‘This is why we’re see-

ing tissue mills move more towards

virgin fibre to make up for the short-

fall in supply,’ McNamara adds.

Better collecting and sorting of old

newspaper grade (ONP) is becoming

more important as supply falls.

Demand for the grade, mostly used in

building materials and cardboard

packaging, has been dropping rapidly

for over ten years. Today, ONP makes

up less than 40% of total recovered

fibre in the US and Canada.

MIXED AND OCC

Mixed paper, which has always been a

‘catch-all category’ has seen ‘pretty

flat’ domestic demand, with almost

no change since 2014. However,

export demand has fallen rapidly,

sparked by China’s National Sword

campaign, followed by other Asian

players unhappy they were ‘importing

garbage’. With domestic demand sta-

ble, the grade has witnessed an over-

all fall of around 4.5% per year.

The most popular grade remains

OCC, which makes up around 70%

paper recycling market. Demand is up

5.8% in 2024 after two weak years.

‘Finally a rebound,’ exclaims

McNamara. ‘Mostly driven by new

capacity (roughly 3.7 million tonnes)

that came online in North America in

since 2019, with the bulk of it added

in 2023 and 2024. We have many new

mills running at full speed now.’

The analyst remarks that recycled

OCC has replaced 2.5 million tonnes

of virgin material. Even so, the indus-

try is expecting more mill closures this

year, following a string at the end of

2024. They involve both virgin and

recycled paper mills.

ANOTHER US-ASIA TRADE WAR?

Last year, Asia’s total

recovered paper

imports fell by about

50% due to a signifi-

cant increase in con-

tainerboard produc-

tion in the region,

according to market

analyst Hannah Zhao

of Fastmarkets RISI.

Mills favoured domes-

tic material to keep

production costs lower.

This trend reduced

European recovered

paper exports by

approximately 20%,

she said, and the end

was not in sight amid

concerns over US tariff

concerns.

In the wake of China’s National Sword policy, India, Malaysia, Thailand, Vietnam and

Indonesia have become a major market for US exports of recovered paper. Zhao reports

these countries bought around 43% (25 million tonnes) in 2023, although this declined to

40% (20 million tonnes) last year. Imports from Europe were at 36%.

India and Vietnam are the biggest importers, purchasing 7.8 million tonnes and 4.7 million

tonnes in 2023, respectively, but down to 5.9 million tonnes and 4 million tonnes in 2024.

Malaysia is the fastest-growing importer, taking 1.8 million tonnes in 2022, 3.5 million

tonnes (up 83%) in 2023 and four million tonnes in 2024 (up 18% surge).

Laos and Taiwan Two are also increasingly important countries. The Asian ‘substitute’ mar-

kets also import 10% and 5% of recovered paper from Japan and Oceania annually.

Zhao points out that over one third of the material these countries process ultimately bene-

fits Chinese containerboard production, meaning it still has a key position on the scrap mar-

ket. She argues that if Chinese demand for recycled paper shrank further, it would greatly

reduce Asia’s overall demand for US and European exports.

Zhao revisits the Us-China trade war of 2019 and says the new US tariffs on Chinese goods

could very well slow the latter’s economic growth (5% in 2024) as well as its demand for

paper packaging and recycled materials.

Data published before the tariffs were announced put China’s paper packaging market value

at US$ 91 billion (EUR 82 billion) this year. Analysts had anticipated 4.5% annual growth in

China’s recycled containerboard sector in until 2027.

The global recycled paper packaging market is currently worth US$ 238.5 billion. It’s ques-

tionable how much further these market figures will fracture – both in China and elsewhere.

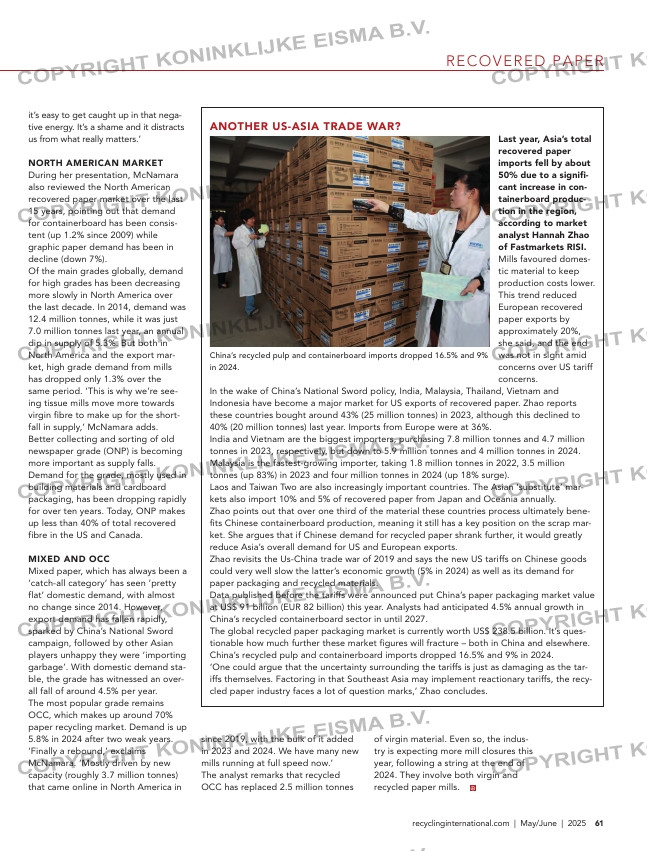

China’s recycled pulp and containerboard imports dropped 16.5% and 9% in 2024.

‘One could argue that the uncertainty surrounding the tariffs is just as damaging as the tar-

iffs themselves. Factoring in that Southeast Asia may implement reactionary tariffs, the recy-

cled paper industry faces a lot of question marks,’ Zhao concludes.

China’s recycled pulp and containerboard imports dropped 16.5% and 9%

in 2024.

58-59-60-61_altpapiertag.indd 61 10-04-2025 14:22